Entry

Reader's guide

Entries A-Z

Cointegration

When a linear combination of nonstationary variables is stationary, the variables are said to be cointegrated, and the vector that defines the stationary linear combination is called a cointegration vector. A time series is stationary if its distribution does not vary over time. The simplest example of a stationary process is {εt} = …,ε-1, ε0, ε1,…., which represents a sequence of independent and identically distributed random variables. The subscript t refers to time. If the distribution of a variable depends on t, it is nonstationary. In cointegration analysis, the most common form of nonstationarity is that of the integrated variables. The random walk, Xt = Xt-1 + εt = X0 + Σti = 1 εi, is an example of a nonstationary variable that is integrated of order one. The word integration refers to the cumulation of epsilons.

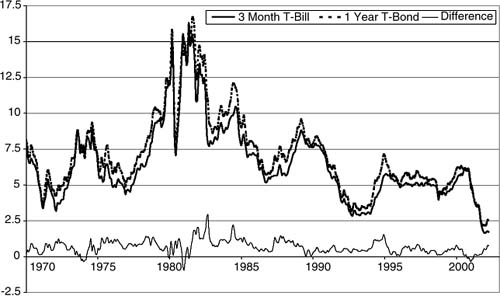

Figure 1 The Interest Rates on a 3-Month Treasury Bill and a 1-Year Treasury Bond for the Period From January 1970 to April 2002

NOTE: The two interest rates appear to be nonstationary, whereas the difference between them seems to be stationary, so the two interest rates are cointegrated.

The concept of cointegration is interesting because it can be applied to uncover relationships that may have theoretical interpretations. For example, the cointegration relations may be defined by the first-order conditions of an economic model, and cointegration analysis can be used to estimate economic models and test certain theoretical hypotheses.

The classical example on cointegration is about a dog that follows its drunk owner. In this example, the positions of the dog and its owner, as a function of time, are two nonstationary processes because the drunk owner is walking around, taking steps in random directions. However, the two processes are cointegrated because the distance between dog and owner is stationary.

Another example is a property of interest rates on bonds with different maturities. Individually, they may have large fluctuations, but the difference between them appears to be stationary. This is illustrated in Figure 1, which contains the interest rates on a 3-month Treasury bill and a 1-year Treasury bond for the period from January 1970 to April 2002. The thin solid line is the difference between the two interest rates.

Historical Development

Cointegration was introduced by Clive W. J. Granger (1981, 1983), and the statistical analysis of cointegrated processes was formalized by Robert F. Engle and Granger (1987), Søren Johansen (1988, 1991), and Peter C. B. Phillips (1991). Cointegration is related to many concepts of ECONOMETRICS, such as unit root processes, spurious regression, and common stochastic trends (for an excellent review, see Watson, 1994). Today there is a voluminous literature on cointegration and applications of cointegration. Recent developments have been on improving and generalizing existing techniques, such as bias and Bartlett corrections; fractionally cointegrated processes; seasonal cointegration; panel cointegration; nonlinear cointegration; and cointegration in relation to processes with structural changes. Many references can be found in the book by James D. Hamilton (1994), which also contains a good introduction to cointegration. Excellent textbooks on likelihood analysis of cointegration are Johansen (1995) and the companion book by Peter R. Hansen and Johansen (1998).

...

- Analysis of Variance

- Association and Correlation

- Association

- Association Model

- Asymmetric Measures

- Biserial Correlation

- Canonical Correlation Analysis

- Correlation

- Correspondence Analysis

- Intraclass Correlation

- Multiple Correlation

- Part Correlation

- Partial Correlation

- Pearson's Correlation Coefficient

- Semipartial Correlation

- Simple Correlation (Regression)

- Spearman Correlation Coefficient

- Strength of Association

- Symmetric Measures

- Basic Qualitative Research

- Basic Statistics

- F Ratio

- N(n)

- t-Test

- X¯

- Y Variable

- z-Test

- Alternative Hypothesis

- Average

- Bar Graph

- Bell-Shaped Curve

- Bimodal

- Case

- Causal Modeling

- Cell

- Covariance

- Cumulative Frequency Polygon

- Data

- Dependent Variable

- Dispersion

- Exploratory Data Analysis

- Frequency Distribution

- Histogram

- Hypothesis

- Independent Variable

- Measures of Central Tendency

- Median

- Null Hypothesis

- Pie Chart

- Regression

- Standard Deviation

- Statistic

- Causal Modeling

- DISCOURSE/CONVERSATION ANALYSIS

- Econometrics

- Epistemology

- Ethnography

- Evaluation

- Event History Analysis

- Experimental Design

- Factor Analysis and Related Techniques

- Feminist Methodology

- Generalized Linear Models

- HISTORICAL/COMPARATIVE

- Interviewing in Qualitative Research

- Latent Variable Model

- LIFE HISTORY/BIOGRAPHY

- LOG-LINEAR MODELS (CATEGORICAL DEPENDENT VARIABLES)

- Longitudinal Analysis

- Mathematics and Formal Models

- Measurement Level

- Measurement Testing and Classification

- Multilevel Analysis

- Multiple Regression

- Qualitative Data Analysis

- Sampling in Qualitative Research

- Sampling in Surveys

- Scaling

- Significance Testing

- Simple Regression

- Survey Design

- Time Series

- ARIMA

- Box-Jenkins Modeling

- Cointegration

- Detrending

- Durbin-Watson Statistic

- Error Correction Models

- Forecasting

- Granger Causality

- Interrupted Time-Series Design

- Intervention Analysis

- Lag Structure

- Moving Average

- Periodicity

- Serial Correlation

- Spectral Analysis

- Time-Series Cross-Section (TSCS) Models

- Time-Series Data (Analysis/Design)

- Trend Analysis

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches